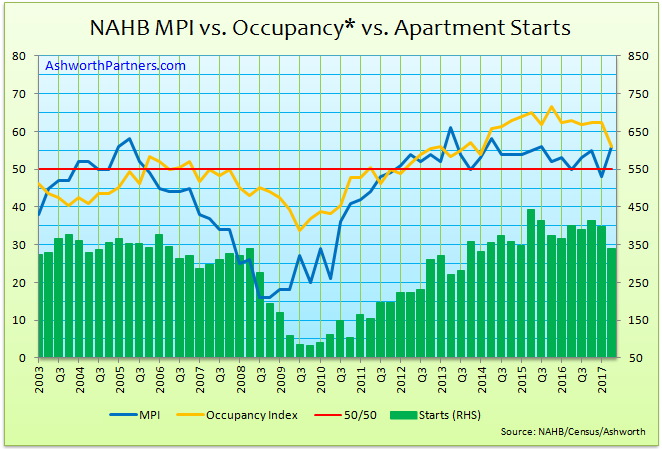

Are apartment builders better predictors of the Apartment Building Investment Cycle? Based on the latest cycle at least (a sample of one, admittedly) it appears that they are.

The National Multifamily Housing Council’s NMHC Quarterly Survey is out now and three of the four categories held fairly steady but the availability of debt financing dropped twenty five points from sixty to thirty five. A reading below fifty indicates worsening conditions and the report on the survey said that with Continue reading Apartment Financing Hits An Air Pocket in Latest NMHC Survey

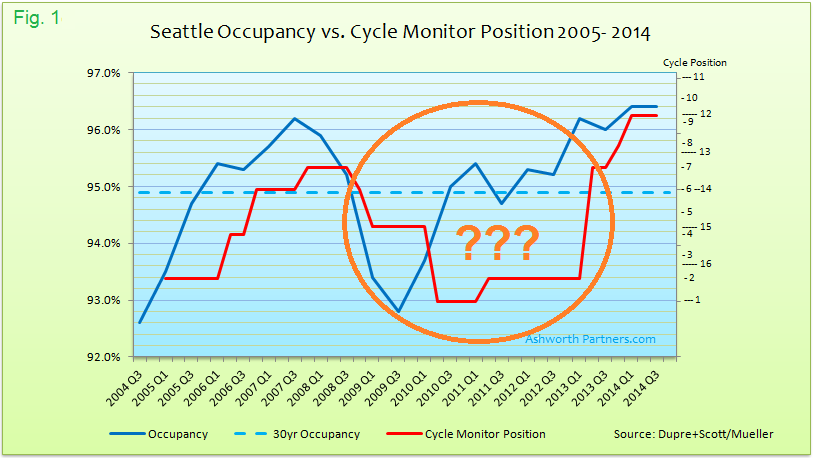

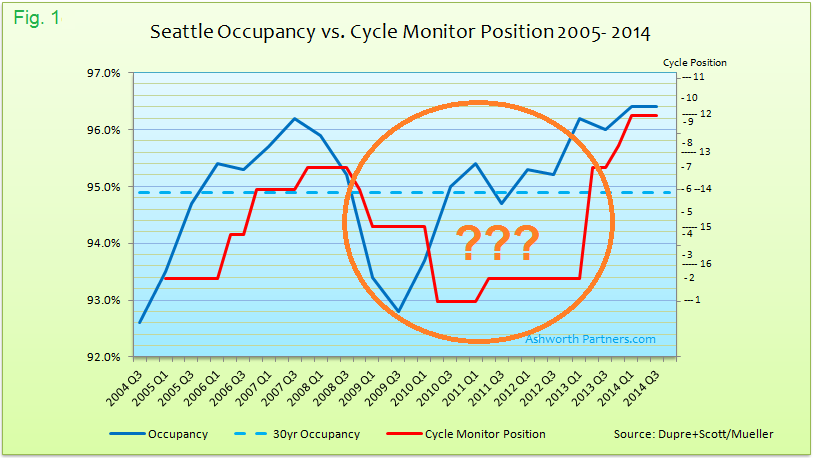

Seattle’s Strange Trip Through the Apartment Building Investment Cycle Part II

In part I we saw that some of the most widely followed market cycle research can’t be relied on without question. If knowing where we are in the market cycle is the most important thing (and not everyone agrees, see the comments from one of my private equity guys about that under part I here) then the best solution is probably to chart the cycles for the markets we’re investing in ourselves. If you’re in multiple CRE sectors in a lot of markets hopefully you have someone on your team or can hire a consultant (like Ashworth) to chart those cycles.

The Strange Tale of the Seattle Apartment Building Investment Cycle and Maybe Yours Too.

Back in 2012 it appeared that Seattle’s movement through the real estate cycle was stalling out. Not the actual market by any stretch of the imagination but instead where it was placed on the apartment market cycle charts in the Cycle Monitor report from Dividend Capital Research. These quarterly reports on the real estate market cycles for the five main Commercial Real Estate (CRE) sectors in more than fifty markets around the US were widely followed but something was wrong.

Click on images for full size.

Why this up to date market data is vitally important to your investment success:

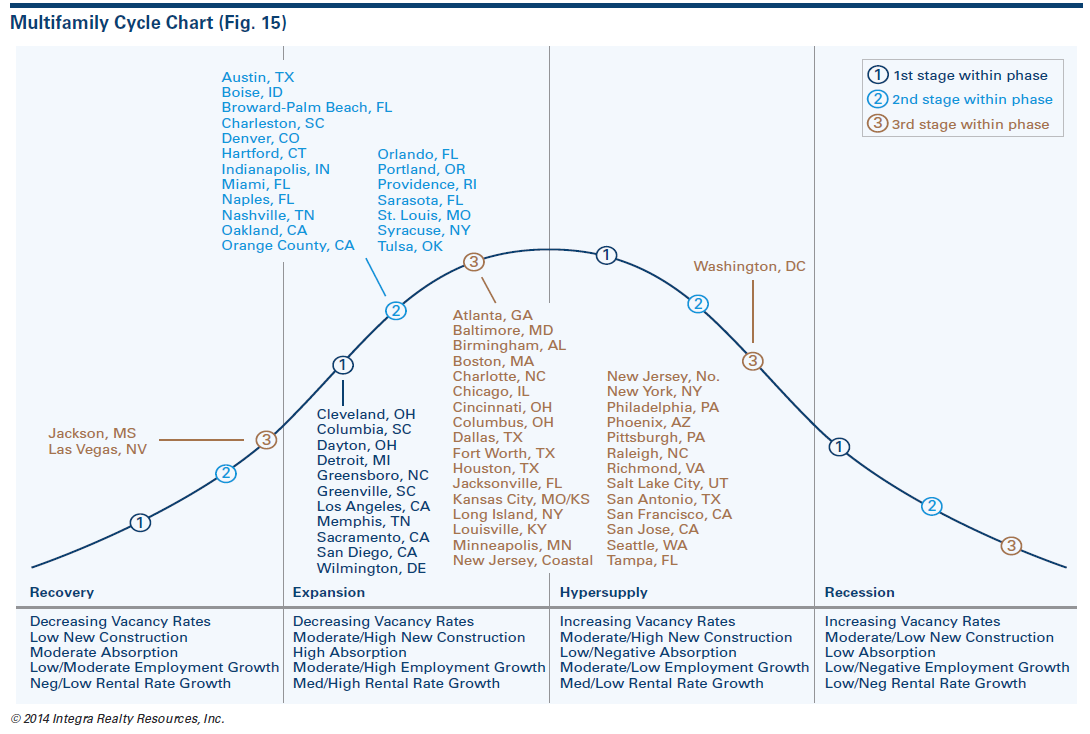

Well Integra Realty Resources (IRR) is just out with their 2015 Viewpoint Report covering where they think things are and where they might be headed in the five major sectors of Commercial Real Estate (CRE); office, industrial, retail, multifamily and hospitality… as well as a bonus piece on self-storage. IRR is one of the largest independent commercial real estate appraisal firms in the U.S and this is their 25th annual IRR Viewpoint in the fifteen year history of the company according to their chairman in his introduction. Not sure on the math there but I do have their reports going back to 2002.

In the report they cover cap rates, going-in cap rates, discount rates, yields, reversion rates and much more but the first thing I look at is their market cycle chart for the multifamily sector:

Click on image for full size. Source: Integra Realty Resources

So IRR has an idea of where your apartment market is, provided your market is in one of the sixty plus places where they have an office. The big question is do you agree with their placement? It is very important to review the data and form your own idea on this because there are good reasons to doubt Continue reading Do You Know Where Your Apartment Market Is Right Now?

First is about the bombshell quote from above. Linneman said there are many studies about home buying that show the down payment is the issue not the mortgage payment and disputes the whole people buy a monthly payment thing.

If I don’t have the downpayment it doesn’t matter what the interest rate is.

Young people are having a very hard time saving for a downpayment at zero percent interest and their parents and grandparents can’t afford to help at zero percent interest on their savings either. Linneman summed it up by putting it in a golfing context: It’s not the green fees it’s the club membership that make it expensive. Japan is the poster child for this bad policy, they’ve been doing QE for twenty five years and it’s done nothing to fix their problems.

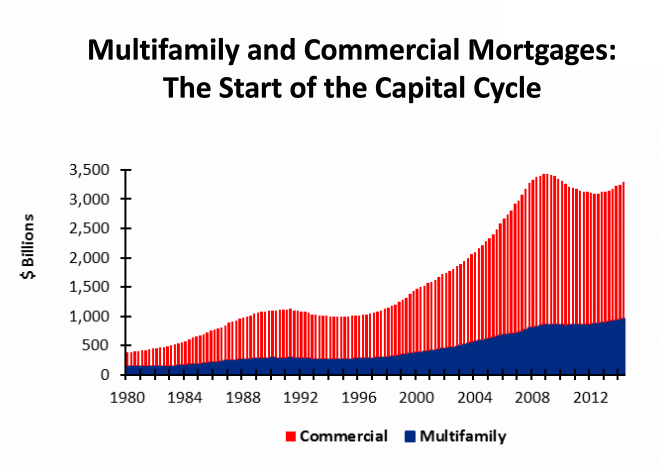

The most interesting thing from a multifamily perspective was that he believes we’re at the beginning of the capital cycle for CRE including apartments:

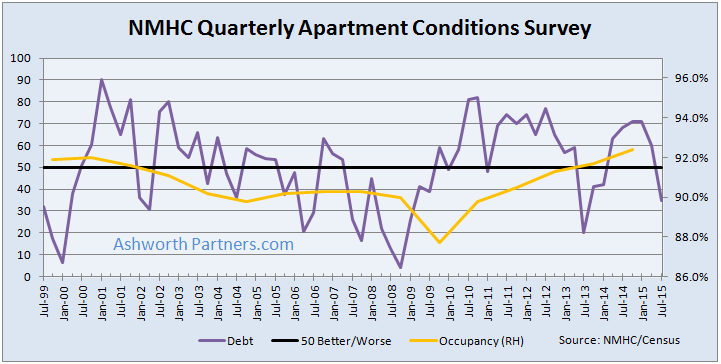

The National Multihousing Council’s (NMHC) latest apartment investment survey out today has market tightness falling to 52 from 68 last quarter. With 50 representing the better vs. worse divide, results show respondents are feeling the bite of new supply plus a bit of seasonal slowdown as well I sense:

Source: NMHC

While the Sales Volume and Debt Financing measures both improved, Equity Financing also slipped. As you can see from the charts above the results tend to be noisy and I suspect that with the survey format it carries a few behavioral biases as well. You can see that the world was ending according to Continue reading Apartment Market Tightness, Equtiy Financing Slide Backwards in Latest NMHC Survey

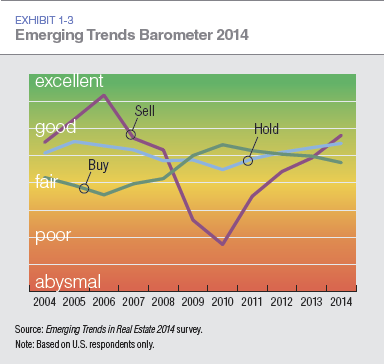

The Urban Land Institute/PriceWaterhouseCoopers annual report on Emerging Trends for Real Estate 2014 was released last week and apartment building investors and commercial real estate pros have some good things to look forward to next year. Note that this post refers to the Americas version of the report with separate sections on Canadian and Latin American markets but they also publish Asia-Pacific and European editions as well. This is the 35th edition of the report is it’s based on individual interviews or surveys from more than 1,000 investors, fund managers, developers, property companies, lenders, brokers, advisers, and consultants.

Here are the 5 key trends we should all be aware of with my comments:

Survey participants continue to rank private direct real estate investment as having the best investment prospects. Pretty expected from this group but the National Council of Real Estate Investment Fiduciaries (NCREIF) recently released its property performance index for the third quarter of 2013 and on a trailing 12-month basis, the index’s return was 11.0 percent, split about 50/50 between income and appreciation. A pretty nice return compared to fixed income rates and a much safer looking bet than buying equities at their all time highs.

Dependence on cap rate compression to drive value is being replaced by an emphasis on asset management. Especially in the 24 hour gateway markets apartment building cap rates are about as low as they can get (well until you look at Vancouver BC) so property performance has to come from actually making the property perform. You also have the problem of what to do with your proceeds if you do sell, as you would be reinvesting right back into the same cap rate market that you sold in… unless you changed to a higher cap rate sector, suburban strip centers anyone?

Opportunities to develop property are finally appearing in sectors other than multifamily. CBRE Econometrics had a piece out last week showing that large (> 350k sf) warehouse properties are being snapped up as fast as they’re being built. Maybe developers who moved over to doing apartments the last few years will move back to their home sectors and ease off on the new supply of multifamily units.

Value-added investment ranked highest in terms of investment strategy; distressed properties and distressed debt ranked last. We were licking our chops a few years ago waiting for RTC 2.0 fire sales to begin and while we were able take down some bank owned inventory, the anticipated tsunami of defaults on commercial loans never materialized. At this point most everything has been extended and pretended into performing status or sold off and so it’s back to making money the old fashion way: Finding and/or creating value.

Both equity investors and lenders are widening their search for business to include secondary markets and niche property types. This will be a double edged sword for investors who are focused on those secondary and tertiary markets as debt financing will be more available but there will also be more competition from sophisticated outsiders with deep pockets. The key will be to make them your buyers so dig in, find the right properties and tie them up quickly.

A lot of the usual suspects when it comes to multifamily markets have moved pretty far into their cycles and if your home area is like ours ti’s getting pretty fully priced. With our value investor mindset that means we’re looking for the next markets to do well over the coming 10-20 years. As apartment building investors we say:

We all know that jobs are a critical driver of the apartment building investment cycle and so we dutifully follow along with the talking heads when the unemployment number is estimated, released and then its potent debated. But Mike Scott over at Dupre+Scott points out in a piece posted Friday that apartment building investors should be following employment, not unemployment. Specifically he recommends measuring how many jobs it takes to create demand for one apartment unit. Currently in King County (where Seattle is the county seat and where Dupre+Scott is located) it takes about 8 jobs to do that:

Source: http://www.duprescott.com Note that we compressed Mike’s four charts into one for brevity.

The formula is simple: Net new jobs / apartment units absorbed. And if you’re an multifamily investor in the tri-county area (King, Pierce and Snohomish in WA State) that Dupre+Scott provides apartment investment research for, they’d be happy to supply you this information http://www.duprescott.com.