Was on NAI Global’s call with Peter Linneman, their chief economist who had some very interesting things to say for apartment building and commercial real estate investors yesterday. Note he’s an actual real estate guy as well as a Wharton professor and I would have lobbied for a better job title at NAI with his background.

First is about the bombshell quote from above. Linneman said there are many studies about home buying that show the down payment is the issue not the mortgage payment and disputes the whole people buy a monthly payment thing.

If I don’t have the downpayment it doesn’t matter what the interest rate is.

Young people are having a very hard time saving for a downpayment at zero percent interest and their parents and grandparents can’t afford to help at zero percent interest on their savings either. Linneman summed it up by putting it in a golfing context: It’s not the green fees it’s the club membership that make it expensive. Japan is the poster child for this bad policy, they’ve been doing QE for twenty five years and it’s done nothing to fix their problems.

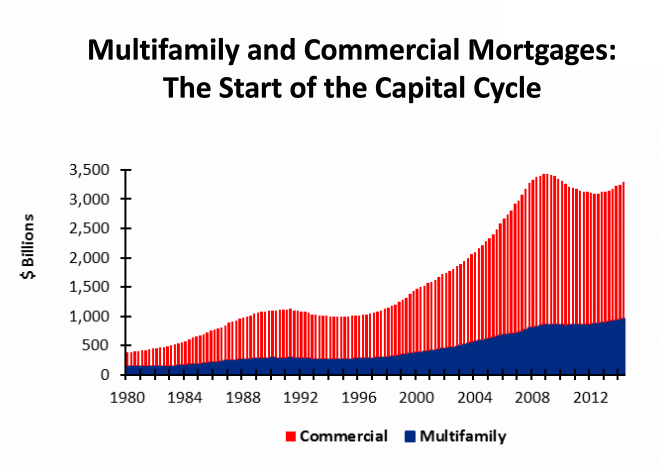

The most interesting thing from a multifamily perspective was that he believes we’re at the beginning of the capital cycle for CRE including apartments:

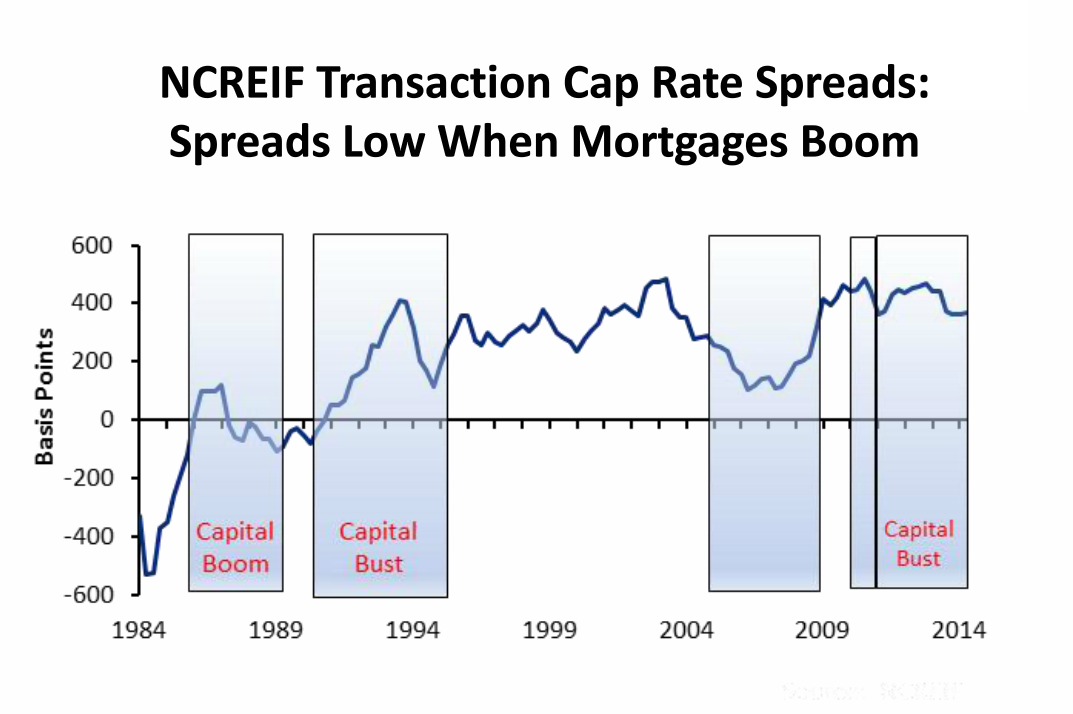

He also believes that cap rates will have a downward trend because as lending picks up cap rate spreads will narrow and he doesn’t believe interest rates are going to be rising as much as everyone seems to think:

Linneman has much more to say (and the research to go with it) on this effect in the Fall 2014 edition of the Linneman Letter.

Good hunting-

In the mid-2015 commercial real estate market in Florida, cap rates have certainly narrowed. 4-5% caps on convenience store NNN land leases??? 5% caps on grocery anchored retail (with way too much “shop space”). Prices aren’t making sense again. Feels too much like 2007!!

That said, the 10 year bond has skyrocketed the last 3 months. Who knows what’ll happen. One of the REIT’s that we represent are no longer throwing money at investors/landlords like they were just six months ago…just can’t justify the very low upside the property will have when they go to sell in 5-7 years… Retail Solutions Advisors

I understand. Hopefully they will have an improved version of the QE over here in Europe.

I recently read that maybe instead of QE there should be a better “public” help, meaning that for instance, some government initiatives could help out with loans or better rates. That’s what some economists say that it would help here in Europe. Something like in this line I read at an opinion article in El Pais from Joseph E. Stiglitz. Cheers.

Ricardo, ideally you are correct that it’s the borrowers who need help not the banks because it’s the borrowers (businesses and homebuyers) who make the economy recover. The problem is that Central Bankers, whether they’re at the Fed, the ECB or the Bank of Japan (BOJ) are bankers first so I believe in their minds saving the banks is the most important thing. The thing that happened with QE in the US was that the Fed made money essentially free to the banks but couldn’t force them to lend it out, bankers made bigger bonuses by using that money for trading and arbitrage than they would have by lending it out for productive uses. Whether that happens in Europe will be interesting to see.