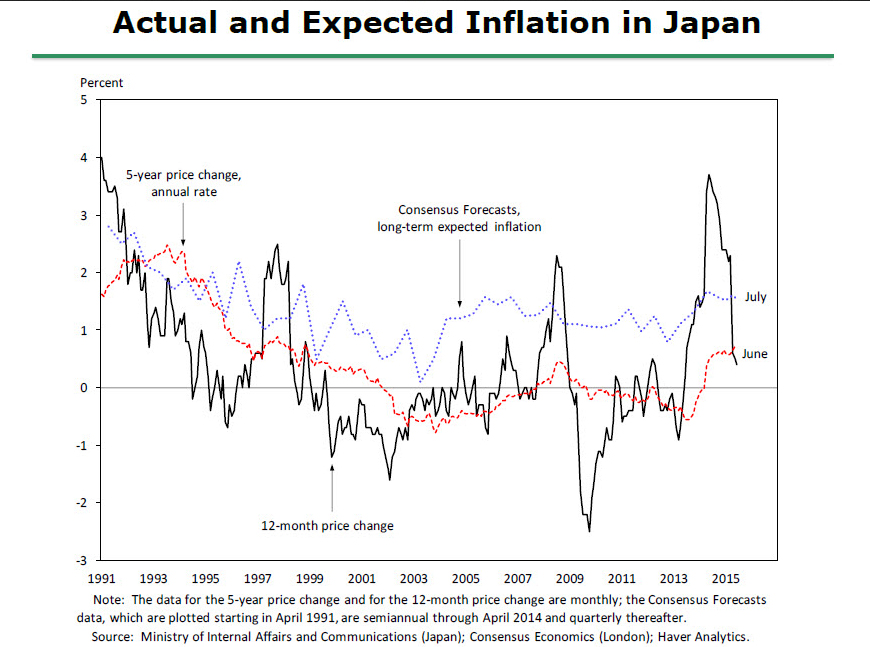

“Here, Japan’s recent history may be instructive: As shown in figure 9, survey measures of longer-term expected inflation in that country remained positive and stable even as that country experienced many years of persistent, mild deflation.” – Janet Yellen Sep. 24, 2015

Was talking about this just last week (again):

As a value guy like you it’s hard to figure out how buying something in the sixes on cap rate works out to be a good deal. But what if the Fed is trapped at the Zero Lower Bound and we are turning Japanese? Their ‘Lost Decade’ is now old enough to graduate with a Master’s degree and we’re following the exact same playbook. I offer last week’s Fed decision as exhibit #1. They would dearly love to raise rates just to prove they can but there’s just thin ice between us and

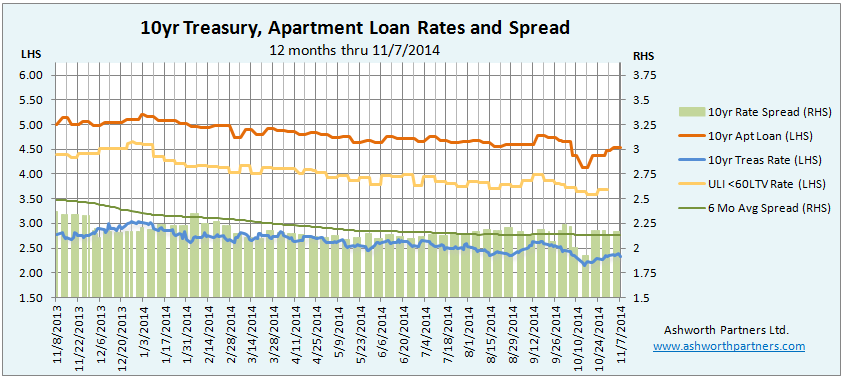

The 10 year apartment building investment loan rate we track moved up to 4.454% from 4.375% yesterday after flatlining at the old rate since the middle of January:

Even so it is still below what we used to think of as the 4.5% floor for this rate. Meanwhile the ULI rate has been tracking the 10yr Treasury, rising from 3.37% April 20th to 3.76% yesterday, a climb of almost 40 basis points.

Is this the beginning of the long anticipated (The 3rd or 4th year in a row that everyone’s known rates were going to rise) rate hikes? It makes sense that the Fed would like them to get up off the floor if for no other reason that they would have room to lower them again when they needed to. But is now the time to do that when China, Europe and the rest of the world are slowing down?

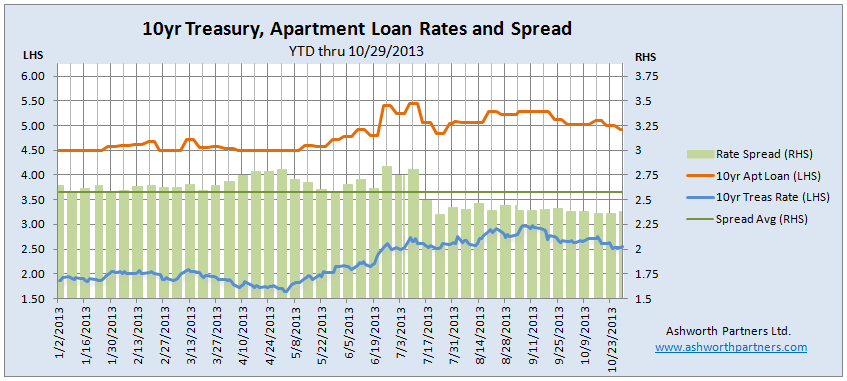

What a month it was for apartment building investment loan rates. The week we were all wondering How is Columbus Day Still a Thing? The 10yr rate we track fell to a low of 4.139% with the spread between it and the 10yr Treasury (T10) breaking below 2% to 1.929 (See below for details on both). I have to hand it to the ULI, they’re good. They had just said:

It only lasted a week but the rate stayed below 4.5% through the end of the month:

As you can see, that one week the spread was also well below its six month average while the T10 got as low as 2.15%, territory it hadn’t seen since the middle of June 2013. We finally got some updated numbers on the ULI rate which would have been nice to have in real time as it was stepping down consistently for six weeks starting in the middle of September, foreshadowing the Continue reading The Great Columbus Day Apartment Loan Rate Massacre and other interesting interest rate stories

In more good news for apartment building investors, both the 10 year Treasury and apartment loan rates have moderated since the Fed’s “non-taper” announcement in mid-September. The spread between the T10 and the 10 year apartment loan rate we track has come in as well. Since 9/16 the Treasury has drifted down from 2.88% to yesterday’s quote of 2.53% while the loan rate has moved from 5.282 down to 4.921, bringing the spread in to 2.381 from 2.402. The average spread for 2013 has also narrowed to 2.573%:

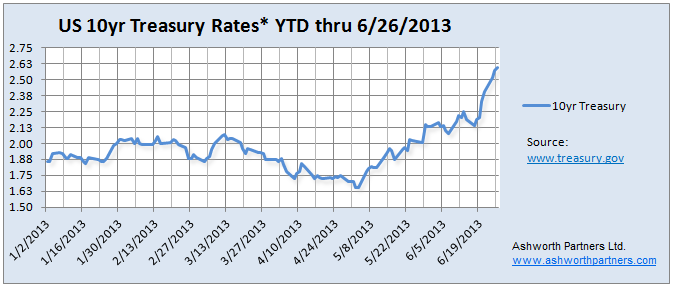

In the Analysis on Tapering QE3 post Tuesday I included a chart of the US 10 year Treasury rates and you could see them going vertical in the days since the Fed announcement and Bernanke’s press conference last week. We’re in the middle of negotiations on an apartment acquisition with a client and so what interest rates do over the next few days and weeks is extremely important to us. So here’s the updated chart:

Click for full size image. *Treasury Yield Curve Rates, commonly referred to as “Constant Maturity Treasury” rates, or CMTs. This method provides a yield for a 10 year maturity even if no outstanding security has exactly 10 years remaining to maturity. More at www.treasury.gov

Bill McBride over at Calculated Risk stares at this stuff all day and has a pretty good track record reading the Fed’s tea leaves. He believes that actual ‘tapering’ of QE3 purchases most likely won’t start before December although there is a slight possibility that it could happen in September if…..

3rd Qtr. GDP rose enough to make 2013 growth look like it will hit the low to mid 2% range.

Unemployment would have to dip enough to make it likely to get down to 7.2%-ish by year end.

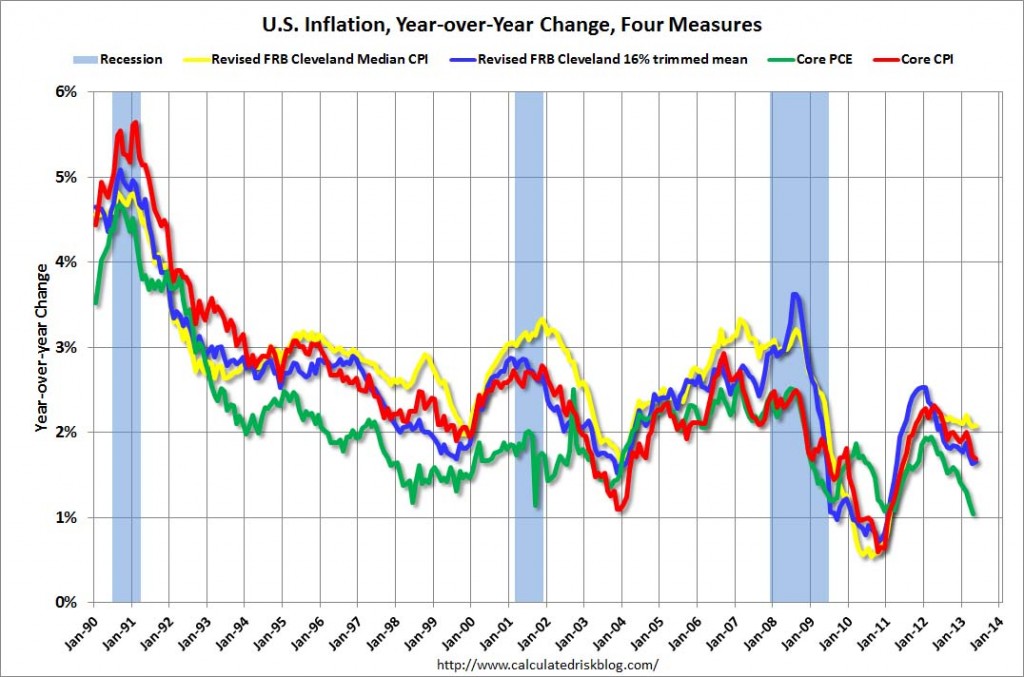

Inflation has to be increasing. Currently the trend is in the wrong direction and Q1 produced only .3% which is well below the 2% annual the Fed Wants.

See Bill’s analysis here: Analysis on Tapering QE3 I highly recommend following Bill’s blog and this is just one of several posts in the last week on Fed comments around the end of tapering. Here’s the inflation chart he posted last week showing four different measures of inflation, note the trend since the beginning of the year:

Click on image to go to Calculated Risk article with chart.

James Montier, who works at the intersection of value investing and behavioral investing (Author of ‘The Little Book of Behavioral Investing’ http://amzn.to/X9Olzc on Amazon among others) has a great quote in his latest white paper published by GMO Global Investment Management entitled “The 13th Labour of Hercules:Capital Preservation in the Age of Financial Repression” Note that you may have to register at the site (free).

His paper discusses the effects of financial repression on portfolio stock and bond allocations and by implication the effects on real estate and particularly apartment building investments. Financial repression is the term used to describe central bank’s strategies for forcing interest rates to zero or negative to spur investment and spending at the expense of saving. Take it away James:

William McChesney Martin was the longest-serving Federal Reserve Governor of all time. He is probably most famous for his observation that the central bank’s role was to “take away the punch bowl just when the party is getting started.” In contrast, Bernanke’s Fed is acting like teenage boys on prom night: spiking the punch, handing out free drinks, hoping to get lucky, and encouraging everyone to view the market through beer goggles. [Emphasis mine]

The paper goes into depth on the effects of financial repression on investments, which grow the longer the repression lasts, up to twenty years. Does the phrase: “… for an extended period” ring a bell? How about QE1, QE2, QE3, and now QE-infinity?