The 10 year apartment investment loan rate we track eased 5 basis points (bp) this week to come in at 4.53%. Both it and the benchmark 10yr Treasury (T10) had been rising since early September and the apartment rate had gotten as high as 4.58% last week before backing off this week.

Despite so many predictions of rising rates we can see that since the election almost a year ago the T10 and the apartment rate have been in a flat to slightly downward trend. Anyone who was alive during the double digit rates of the seventies and eighties has it almost hardwired in their mind that rates must go back up, right? But with slowing population growth, plunging workforce participation and modest productivity growth it’s hard to see what the drivers of inflation and therefore rates would be. Add on banks getting out of business lending, the perverse incentives for corporations to buy back stock instead of investing in plant, equipment or people and falling commodity prices and it isn’t too surprising that economic growth and inflation remain muted.

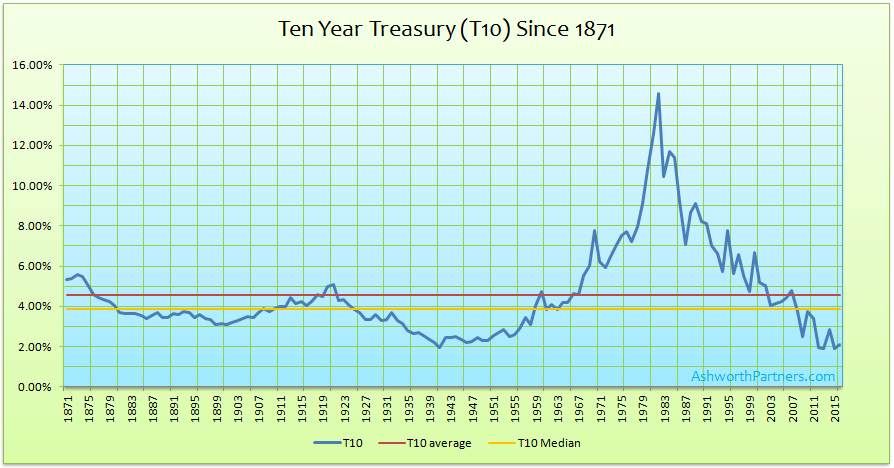

Viewed historically we get a different picture:

We can see that the T10 median is less than 4% which means that it has been below that point for half of its existence. Recency bias (if we can call the last 35 years or so ‘recent’) must be a play in the minds of those who constantly predict higher rates. The fact of the matter is that we’re just 150bp below the median which granted is near the historical lows but if we were to take out the one super inflationary period starting in the late seventies think how low the median would be.

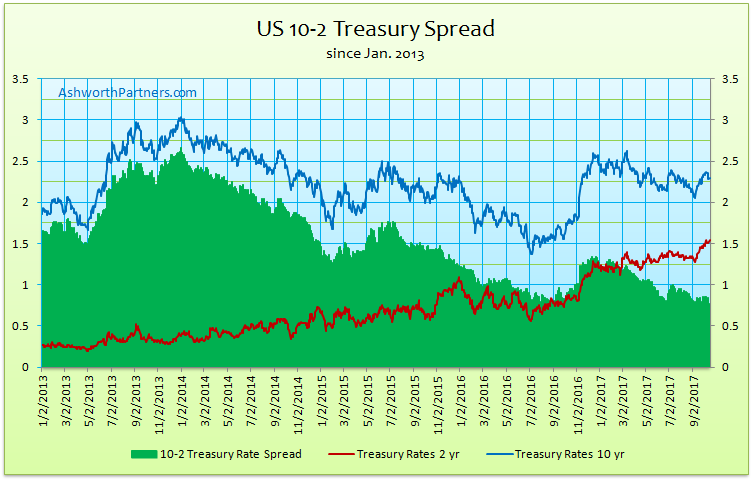

Unfortunately the ULI <60 LTV rate has gone AWOL again and access to the data is beyond the budget of my posting it for free on here. The good news is that next month I will debut a new feature which is tracking the 10-2 spread, the difference between the T10 and the T2 which historically has been very predictive of moves in the economy. Here’s a sneak peak of the chart and next month we’ll dive into the whys, wherefores and what it’s telling us now:

Speaking of the spread between the T10 and the apartment building rate we track, the green line on the chart represents the six months trailing average spread. We track changes in the trend for signs apartment lenders becoming more or less competitive. Note that since rates are only quoted on business days the chart averages the last 120 business days which roughly equates to six calendar months.

We track the 10 year Treasury (T10) because it is the benchmark most lenders base their long term rates on. In order to lure investors away from Treasuries to buy mortgage bonds lenders have to offer a premium (AKA ‘spread’) over what can be earned on the ‘risk free’ Treasury. So when the T10 moves, rates on all kinds of longer term loans including on apartments tend to move also. As you can see in the chart, the spread also widens and narrows as market forces make an impact.

Notes about the apartment loan rates shown in the chart above: The rates shown here are from one West Coast regional lender for loans on existing apartment buildings between $2.5 – 5.0M. The rate quote they send every Monday that I track is a 30 year amortizing loan with a fixed rate for 10 years (They also have other fixed periods at different rates). The max LTV for this loan is 75% (they have an even lower rate on their max 60LTV loans) and the minimum Debt Cover Ratio (DCR, aka DSR or DSCR) is 120. Note too that these are ‘sticker’ rates, LTVs and DCRs and ‘your millage may vary’ depending on how their underwriting develops. I usually figure that we’ll end up at a 70LTV which also helps the debt cover and provides a larger margin of safety, which is half the battle from a value investing standpoint.

The prepay fee is 5,4,3,2,1% for early repayment in the first five years and you do have the ability to get a 90 day rate lock. The minimum loan is $500k (at a slightly higher rate for less than $1M loans) and they’re pretty good to work with as long as you go in knowing that it takes up to 60 days to close their loan. If you are looking at acquiring an apartment building in California, Oregon or Washington I’d be happy to recommend you to my guy there for a quote. Send me a message through this link and I’ll make an introduction for you.

Note that the 15 year rate we track is also a 15 year amortizing loan with very similar terms to the 10yr loan.

The other rate we track is the from the Trepp survey which the ULI (Urban Land Institute) reports on. According to the ULI the Trepp rate is what large institutional borrowers could expect to pay on a 10 year fixed rate, less than 60% LTV loan for a “crème de la crème” core property located in a gateway market. We track this rate as a barometer of what the largest lenders are offering their best customers on the most secure loans for any advanced warning about future rate changes. Note that the spread we chart is between 10yr apartment loan we track and the T10.